- Home

- Double Entry Bookkeeping

- Bookkeeping Journals

Bookkeeping Journals

Bookkeeping journals are where a business records its daily financial transactions in date order showing which accounts to debit or credit with journal entries.

This is much like personal journals in which people record the events that happen in their life in date order.

Bookkeeping journals also go by the name of:-

The information from the bookkeeping journals is transferred to bookkeeping ledgers.

This transfer is called ‘posting’.

The journals show which ledger account should be debited with the transaction amount and which one should be credited with the same amount.

Check out debits and credits for a better understanding of this system.

Journal Types

There are two main types

- General Journal

- Special Journals :

- Sales Journal

- Cash Receipts Journal

- Sales Returns and Allowances

- Purchases Journal

- Cash Payments Journal

- Purchases Returns and Allowances

On this page we will discuss the General Journal and two Special Journals i.e. the Sales and Purchases Journals.

General Journal

The General Journal is the main bookkeeping journal of a business. Most transactions are entered into it.

Information from the General Journal is posted into the main ledger known as the General Ledger.

It is easy to set up a journal in a lined exercise book or computer spreadsheet. You need five columns.

Sample General Ledger Journal Entry :

Sample of a General Ledger Journal Entry

The first line (telephone) is against the margin which means that this ledger account is to be debited.

Notice how the second line (bank) is indented to show that this is the account to be credited.

There is a description line which gives a brief explanation of the supplier’s name and how it was paid.

Once the information has been posted to the ledgers, the last column ‘Ref’, also known as ‘Post Ref’ can be used in two ways:-

- Enter a ‘P’ (for posted), or

- Enter the ledger account number as in the above illustration.

If the P or the account number is not there it would mean the information has not been posted yet.

The next business transaction will be recorded directly below this one by simply skipping one line. The whole page of the General Journal will be filled up in this manner with business transactions as they happen.

Each page of the journal is assigned a number such as J1 for the first page, J2 for the second and so on. This page number will be used as a reference in the bookkeeping ledgers.

Here are some journal entries specific to different types of transactions specific to loans.

Sales Journals

Let’s have a look at an example of an entry in the general journal for a sale on credit (sales that will only be paid for in 30 or 60 days etc.):-

Journal Example a Sale on Credit in the general journal

Note - Accounts Receivable is the ‘control account’ ledger used for recording sales that have not yet been paid for. If the sale was paid for right away the debit account would be ‘bank'.

There is a problem with this type of entry...

... many sales on credit require the entry of repetitive bookkeeping journals which would be tedious. It is better to only have one journal to enter - a summary of all sales on credit - at the end of the month.

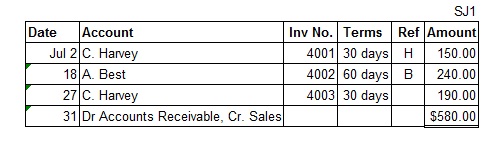

Therefore, it makes sense to maintain a separate journal designed to handle customer transactions... The Sales Journal.

The sales are listed under each other using only one column for the amounts.

This takes away the need to do debit and credit entries and a description line for each and every sale, which greatly reduces time spent on this task.

At the end of the month, the list is totaled and the debit and credit journal entry indicated on the bottom line.

The reference is the first letter of the client’s name (or

surname for an individual), or it could be assigned a number, eg. if the

Accounts Receivable ledger is given the account number ‘003, then

customers could be given the number 003.1, 003.2 etc.

Example of a Journal for a list of different sales on credit

Purchases Journals

These work much the same as sales journals and are used to record

the purchase of items that will only be paid for in 30, 60 etc. days.

Example of a general journal entry for a purchase on credit

Note - Accounts payable is the ‘control account’ ledger used for recording purchases that have not yet been paid for.

If the purchase was paid for right away the credit account would be ‘bank’.

Unlike sales, there are usually many different types of purchases so the Purchases Journal has multi columns to show the detail.

Some types of purchases are made on a frequent basis so these have their own columns.

See the illustration below.

The frequent ones are Purchases, Store Supplies and Office Supplies.

The other purchases that don’t happen so regularly are detailed under the generic ‘Other Accounts’ column

Notice how the account numbers are shown in brackets at the bottom of the columns for the frequent purchases.

Whew! ...and that’s only three of the bookkeeping journals! Your head is probably spinning now with all this information.

Check out these journal entry examples and try your own with this journal entry template in excel.

Bookkeeping Journals Quiz

Take the quiz to test your knowledge on what you just read! Click on Start below.

Got Questions or Want to Leave a Comment?

Contact Me

Track your income and expenses in our free Excel Template, and instantly know your profit.

Latest Posts

-

10 Free Bookkeeping Courses to Understand Business Accounts

These are the best free bookkeeping courses online for anyone in business who must understand business accounts. Learn the bookkeeping language, how to balance the books, how to manage finances, doubl…

These are the best free bookkeeping courses online for anyone in business who must understand business accounts. Learn the bookkeeping language, how to balance the books, how to manage finances, doubl… -

Accounts Receivable Journal Entries

Accounts receivable journal entries: Debit Accounts Receivable, Credit Sales Income, and see other journals for sales returns, discounts, interest and write-offs.

Accounts receivable journal entries: Debit Accounts Receivable, Credit Sales Income, and see other journals for sales returns, discounts, interest and write-offs. -

Accounts Receivable Procedures Step by Step

7 accounts receivable procedures to manage credit sales effectively. Learn the best practices for invoicing, payment collection, and maintaining healthy business finances.

7 accounts receivable procedures to manage credit sales effectively. Learn the best practices for invoicing, payment collection, and maintaining healthy business finances.