- Home

- Bookkeeping Questions

- Insurance Journal Entry

Insurance Journal Entry

A basic insurance journal entry is Debit: Insurance Expense, Credit: Bank for payments to an insurance company for business insurance.

Not all insurance payments (premiums) are deductible* business expenses.

Some insurance payments can go on to the Profit and Loss Report and some must go on the Balance Sheet.

So when it comes to entering these transactions into the bookkeeping records of a business there are different journal entries to consider.

There are various types of insurance cover available to small businesses and business owners so we'll have a look at those and how best to treat them in the accounts.

Plus, there are questions I received from real bookkeepers/business owners who needed to know how to enter their insurance proceeds from property damage to which you can read my answers.

*A deductible expense is one that can be included in your income tax calculations.

Insurance Expense Journal Entry

An insurance expense occurs after a small business signs up with an insurance provider to receive protection cover.

The insurance provider charges an annual fee, called a premium, which will cover the business for 12 months.

This annual fee can be paid with a one-off payment or it can be spread over 12 monthly payments, or sometimes fortnightly.

The annual payment is usually cheaper than the total of the monthly payments as an incentive to pay the bill up-front, but small businesses often can’t afford this, so the providers offer the monthly option.

1. Business Insurance

Here are some common types of insurance that are recommended for a business depending on the type of business they operate.

All of these have the same insurance journal entry:

Debit: Insurance Expenses (expense account) Credit: Cash/Bank (asset account)

General Liability Insurance

This insurance can also be known as public liability insurance and protects against financial loss resulting from other people’s property damage, injuries to people and medical costs, lawsuits and more.

Professional Liability Insurance

This insurance can also be known as professional indemnity insurance and is suited for businesses providing a service. It protects against financial loss resulting from errors or negligence.

Other Insurances

These include commercial property cover, product liability cover and employee cover.

Compulsory Insurance

Some insurances may be compulsory like Worker’s Compensation, Commercial Auto and Professional Liability.

The Small Business Administration, USA has more information on Business Insurance.

2. Motor Vehicle Insurance

A business that owns motor vehicles will require insurance cover on those.

The recommendation is to group this insurance with the other motor vehicle expenses (fuel, r&m) in the bookkeeping accounting records.

So, the vehicle insurance journal entry is:

Debit: Motor Vehicle Expenses (expense account) Credit: Cash/Bank (asset account)

With the right bookkeeping software, the bookkeeper can open sub-accounts under the Motor Vehicle expense account like this:

Motor Vehicle Expenses (Main expense account)

Gas/Fuel

Vehicle Insurance

Vehicle Repairs & Maintenance

A sole proprietor or trader who uses their personal vehicle for business activities needs to select the right type of insurance based upon the type of activity - are you driving yourself to an appointment (the individual insurance may cover you) or are you transporting people for a charge (then you will probably require commercial auto insurance)?

Your individual vehicle insurance may not cover your business use of your personal vehicle and so you will need to ask your insurance provider.

Individual vehicle insurance is not a deductible business expense so the insurance journal entry for individual vehicle insurance, if paid out of the business bank account is:

Debit: Drawings (equity account) Credit: Cash/Bank (asset account)

However, you can then reclaim a portion of that as a business expense when you calculate your deductible vehicle expenses based on the business use of your personal vehicle.

The journal entry for this is:

Debit: Motor Vehicle Expense (expense account) Credit: Capital (equity account)

Capital is the account used for showing how much personal money is used by the business owner to pay for business expenses. It can either be deposited into the business bank account and coded to Capital or presented by a journal like the one above.

3. Personal Insurance Business Owner

Business owner/s may have the following personal insurances:

- Life Insurance

- Health Insurance

- Income Protection

- Trauma

- Disability, and more

The insurance journal entry for business owners is:

Debit: Drawings (equity account) Credit: Cash/Bank (asset account)

The above journal is only used when the business pays for the owner’s personal insurance out of the business bank account.

Personal insurance payments are not deductible business expenses so must not go on the Income Statement (Profit and Loss Report). They must go on the Balance Sheet.

If the business pays for the insurance out of the business bank account and then the owner repays the business, here are the insurance journal entries:

Business Makes Payment:

Debit: Drawings (equity account) Credit: Cash/Bank (asset account)

Owner Repays Business:

Debit: Cash/Bank (asset account) Credit: Capital (equity account)

If the business owner pays for their insurance with their own money, then nothing gets entered to the business bookkeeping records.

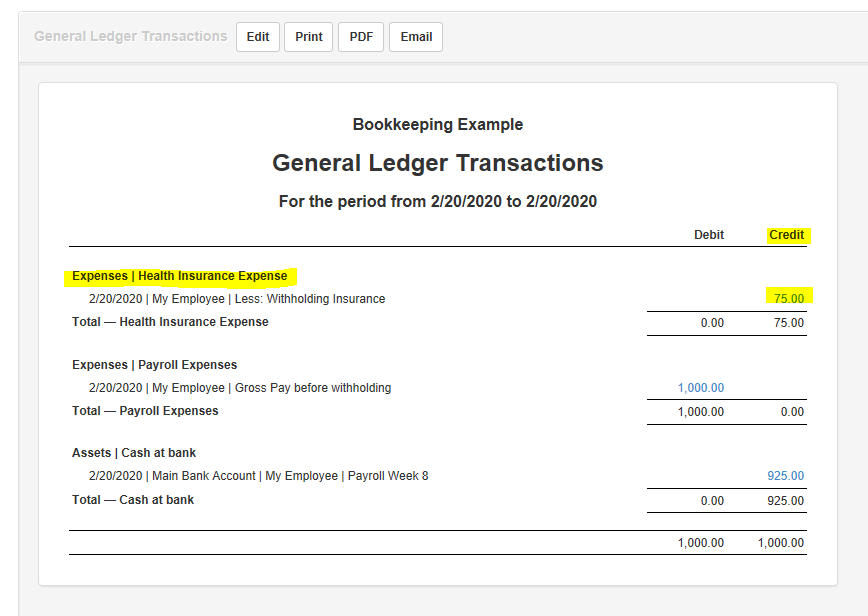

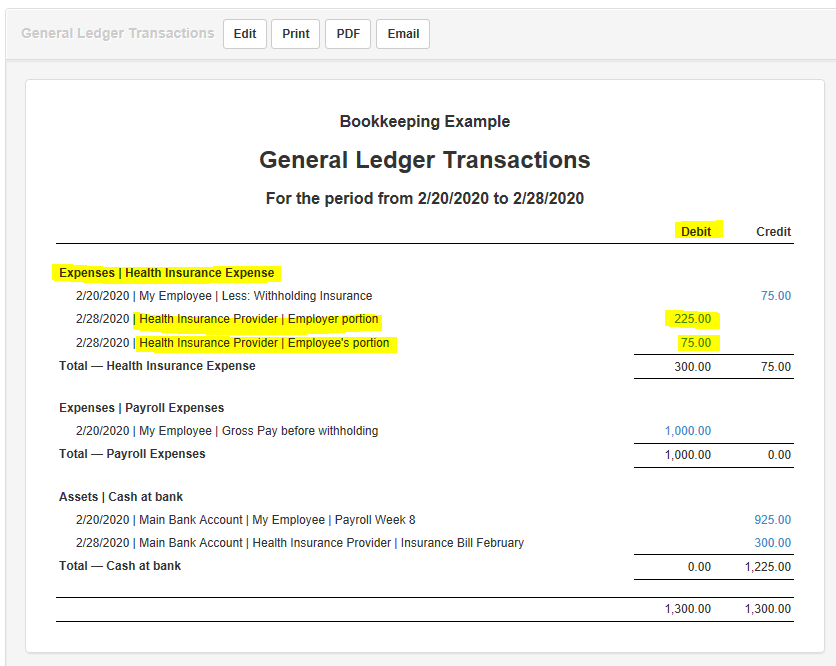

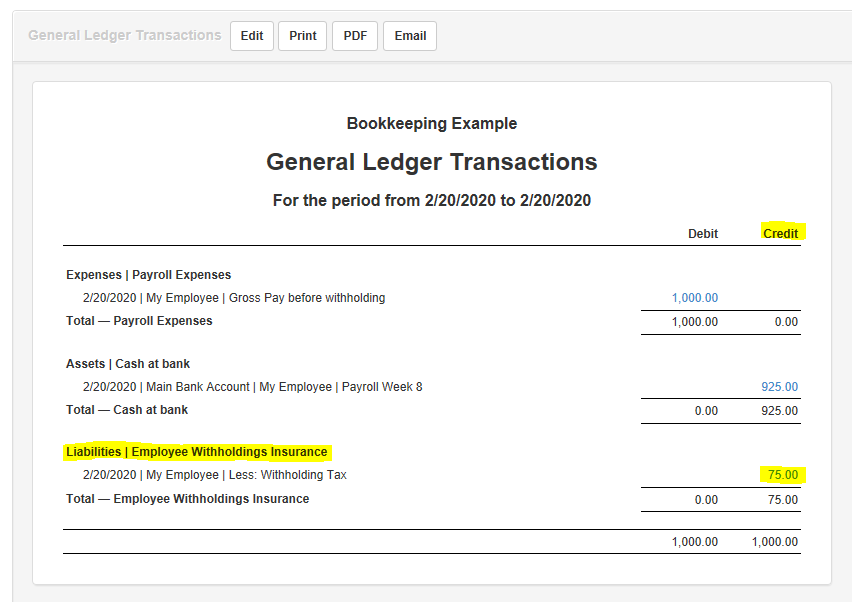

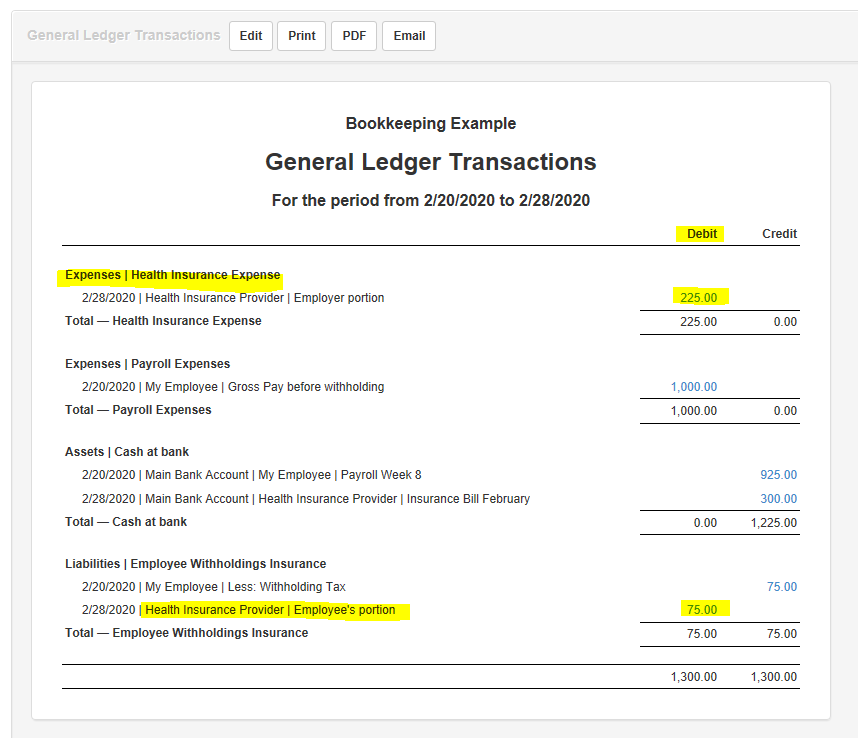

4. Employee Health Insurance

Accountingcoach.com has a good example of accounting for payroll withholdings for health insurance.

I have entered their figures into the free bookkeeping software called Manager so you can see the insurance journal entry in action.

Example 1:

Credit $75 to the Insurance Expense (expense account) for Employee's Withholding

Withholding Insurance in Expense Account

Withholding Insurance in Expense AccountDebit $75 to the Insurance Expense (expense account) for the Payment

Paying Insurance to Insurance Provider

Paying Insurance to Insurance ProviderExample 2:

Credit $75 to the Employee Withholdings Insurance (liability account) for the Withholding

Withholding Insurance in Liability Account

Withholding Insurance in Liability AccountDebit $75 to the Employee Withholdings Insurance (liability account) for the Payment

Paying Insurance to Insurance Provider

Paying Insurance to Insurance ProviderInsurance Journal Entry For Proceeds

1. Individual or Business Owner Proceeds

If the insurance provider pays personal insurance proceeds (like life insurance due to the death of an insured loved one) into your business bank account (because that’s the account you gave them or because that’s where you deposited the check as a sole proprietor), then the journal entry in the business bookkeeping records will be:

Debit: Cash/Bank (asset account) Credit: Capital (equity account)

If you need to draw that money (or some of the money) out of the business for personal use, the journal entry will be:

Debit: Drawings (asset account) Credit: Cash/Bank (asset account)

Debit: Drawings (asset account) Credit: Cash/Bank (asset account)

2. Business Insurance Proceeds

When a business puts in an insurance claim to their provider for damages, the provider will pay money to help them cover the costs of repairing or replacing what was damaged (this is just one example).

These types of payments are called proceeds.

Debit: Cash/Bank (asset account) Credit: Other Income (income account)

The above journal uses the Other Income account to show it is not part of the normal day to day activity income earned by the business.

Another insurance journal entry for proceeds is:

Debit: Cash/Bank (asset account) Credit: Repairs & Maintenance (expense account)

This journal would be used if your business has paid or will be paying a contractor to repair something.

You can see from the above insurance journal entry that the proceeds have been placed into an expense account; this is because it puts the check back into the same account that the original repair payments were made from.

In accounting it is perfectly acceptable to put money received into an expense account to offset (reduce) the original expense.

3. Motor Vehicle Proceeds

For repairs to motor vehicles the insurance journal entry for proceeds will be similar:

Debit: Cash/Bank (asset account) Credit: Motor Vehicle Repairs (expense account)

4. Other Proceeds

There are other ways of dealing with insurance proceeds especially when it comes to inventory - Investopedia explains how to account for that here or high value assets of a business such as buildings like in Question 2 near the end of this article.

Insurance Journal Entry for accounts payable

When you are tracking accounts payable your insurance journal entry will be different to the ones shown further up this page.

When you receive the bill from the insurance provider the journal will be:

Debit: Insurance Expense (expense account) Credit: Accounts Payable (liability account)

Then paying the bill:

Debit: Accounts Payable (liability account) Credit: Cash/Bank (asset account)

In your bookkeeping software you will enter the full cost shown on the bill at the date of the bill. This full amount will go on to the Profit and Loss at that date.

When payment is made, either in full or with monthly payments, the bill will decrease, which means the accounts payable account will decrease.

Once again I have entered an example into the free bookkeeping software called Manager.

The example is a bill of $1,000 for General Liability insurance and then two payments of $84.

Enter Insurance Bill - Debit: Insurance Expense, Credit: Accounts Payable

Two Payments Against Bill - Debit: Accounts Payable, Credit: Bank

Insurance Journal Entry Questions

Question 1

"An employee of our small business damaged our property with her car. The business paid to have the damage repaired and later the employee reimbursed the business with a check from her insurance company. What GL account should this reimbursement go into so that it is not considered income?

Answer:

You can put the insurance check back onto the same expense account that the original repairs were coded to which will offset that expense.

It is acceptable to put money received into an expense account when it makes sense to do so, as it does in this instance.

So, if you originally put the repairs against a Repairs & Maintenance expense account, that is the account you will put the insurance proceeds against.

Here is an article by valuesdrivenresults.com which explains it.

The journal entry is:

Debit: Cash/Bank (asset account) Credit: Repairs & maintenance (expense account)

Question 2

"I am doing the books for a small property management co. The building suffered water damage. The owner received a check from the insurance company. He will now use that to make repairs. How do I book these transactions?

I was thinking:

For the damage:

DR CR

Damage/Exp Asset/Bldg

For the Insurance Check

DR CR

Cash Damage/Exp

When we pay for the repairs:

DR CR

Asset/Bldg Cash

What do you think?

Answer:

I recommend checking with your client’s tax accountant because of the complexities around high value assets and costly damages.

In the meantime, your journals look logical and should make the events clear for anyone to follow.

The Damage/Exp is offset with the insurance check which is fine.

Something to keep in mind is if these two entries are in different months.

If you use an expense account, the P&L will show a huge loss in one month (from the damage) and then a huge profit in the month that the insurance check is received.

I recommend avoiding doing this because these journal entries won’t give your client a true picture of their day to day results.

Instead, use an account on the balance sheet for both entries.

Here are the journal entries that could be done:

For the Damage:

Debit: Damage (liability account) Credit: Buildings (asset account)

For the Insurance Check:

Debit: Insurance Expense (expense account) Credit: Cash/Bank (asset account)

When Repairs Are Paid For:

Debit: Buildings (asset account) Credit: Cash/Bank (asset account)

Another thing to watch for is if the repair costs come to less than the insurance check (unless the insurance company has paid the exact repair quote) - the difference will have to be recorded as income - Insurance Gain - on the P&L.

Here is the insurance journal entry for the insurance check, the credit side is split between two accounts:

Debit: Cash/Bank (asset account) Credit: Damage (liability account) and Insurance Gain (income account)

I am sure if the Accountant wants to change anything, adjusting journals can be done. But in the meantime, these entries will keep the books looking good.

Got Questions or Want to Leave a Comment?

Contact Me

Track your income and expenses in our free Excel Template, and instantly know your profit.

Latest Posts

-

10 Free Bookkeeping Courses to Understand Business Accounts

These are the best free bookkeeping courses online for anyone in business who must understand business accounts. Learn the bookkeeping language, how to balance the books, how to manage finances, doubl…

These are the best free bookkeeping courses online for anyone in business who must understand business accounts. Learn the bookkeeping language, how to balance the books, how to manage finances, doubl… -

Accounts Receivable Journal Entries

Accounts receivable journal entries: Debit Accounts Receivable, Credit Sales Income, and see other journals for sales returns, discounts, interest and write-offs.

Accounts receivable journal entries: Debit Accounts Receivable, Credit Sales Income, and see other journals for sales returns, discounts, interest and write-offs. -

Accounts Receivable Procedures Step by Step

7 accounts receivable procedures to manage credit sales effectively. Learn the best practices for invoicing, payment collection, and maintaining healthy business finances.

7 accounts receivable procedures to manage credit sales effectively. Learn the best practices for invoicing, payment collection, and maintaining healthy business finances.

{kind=link}